Checklist for Choosing a Dental Payment Plan

Dental care can be expensive, and many Australians delay treatment due to costs. Payment plans help break down these expenses into manageable instalments, allowing you to prioritise your oral health. Here’s what to consider when choosing a dental payment plan:

- Understand Your Treatment Needs: Know whether you need general, cosmetic, or specialist care. Costs vary widely – e.g., a routine check-up averages $219, while dental implants can exceed $5,000.

- Calculate Total Costs: Request a detailed quote, including follow-ups and hidden fees like deposits or transaction charges.

- Review Payment Terms: Compare repayment periods (weeks to years), instalment schedules, and interest-free options. Watch for fees like account maintenance or missed payments.

- Check Eligibility: Some plans require credit checks, while others don’t. Ensure you meet age, residency, and income requirements.

- Confirm Provider Coverage: Not all dentists accept all plans. Check your clinic’s partnerships and ensure the plan suits your treatment cost range.

Quick Tip: Always read the fine print to avoid surprises, and consider combining a membership like smile.com.au for fee reductions with a payment plan for larger procedures.

Australian Dental Payment Plans Comparison: Costs, Terms and Coverage Limits

How to Get Affordable Dental Care in Australia Without Money

1. Identify Your Dental Treatment Requirements

Before choosing a payment plan, it’s essential to understand the dental work you need. Ask your dentist for a detailed treatment plan, including ADA item numbers, so you can compare options and clarify what your insurance will cover.

Dental care generally falls into three main categories: general dentistry, cosmetic dentistry, and specialist care. General dentistry includes things like check-ups, fillings, and simple extractions. Cosmetic dentistry focuses on treatments like teeth whitening, veneers, and bonding. Specialist care involves more complex procedures such as orthodontics, implants, and advanced root canals. For example, a routine check-up – covering an exam, scale and clean, and fluoride treatment – costs around AU$219 on average, while a full veneered crown can set you back about AU$1,678[8]. Specialist consultations tend to be pricier, averaging AU$120 compared to AU$67 for general dentists[8]. Understanding your specific treatment needs will help you calculate exact costs and spot any potential extra charges.

1.1 Determine What Type of Care You Need

Figuring out whether your treatment falls under general, cosmetic, or specialist care is crucial. Payment plans and insurance policies often have different coverage limits for each category. General care typically includes preventative and restorative treatments, like fillings (averaging AU$220) or extractions (around AU$205)[8]. Cosmetic and specialist procedures, on the other hand, can vary widely in cost. In Australia, about 8–10% of dentists are specialists across 13 fields[8]. For instance, a full crown done by a specialist averages AU$2,133, compared to AU$1,678 when performed by a general dentist[8].

Once you know the type of care you need, you can start calculating the total financial commitment.

1.2 Calculate the Total Treatment Cost

Ask for a written breakdown of all treatment stages, including follow-up visits and any additional procedures. For complex treatments like dental implants, costs are often split. The initial implant insertion can range from AU$1,334 to AU$3,000, while fitting the abutment adds another AU$400 to AU$1,404[8]. Keep in mind that fees can vary depending on your location.

For procedures such as wisdom teeth removal, make sure the quote specifies whether anaesthetist fees and hospital charges are included, as these are often billed separately. Between July 2020 and July 2022, general dental fees rose by 3.7%[8]. If your treatment isn’t immediate, consider potential price increases. If you have private health insurance, check whether your dentist is a "preferred provider", as this can lower out-of-pocket costs with capped fees and higher rebates.

1.3 Look for Hidden Fees or Exclusions

Some payment plans come with extra fees, such as start-up costs, monthly account maintenance fees, or penalties for missed payments. Transaction fees can also apply, sometimes up to 1.75% per instalment[9]. Additionally, some plans include a "co-payment" surcharge – for example, 3.9% for six-month plans or 5.9% for 12-month plans[9].

Many plans also have minimum treatment costs. Some clinics only offer financing for procedures over AU$3,000[10]. Deposits are typically 10% to 25% of the total cost[9][3][10]. Make sure to clarify whether "interest-free" means no interest throughout the entire period or just during an initial promotional phase. For example, DentiCare offers plans for treatments ranging from AU$50 to AU$12,000[7]. Confirm that your treatment falls within the required range before applying.

2. Review Payment Plan Terms and Options

When it comes to dental treatments, making sure your payment plan fits both your medical needs and your financial situation is crucial. Once you’ve got a handle on the treatment costs, take a closer look at the structure of the payment plan. Repayment periods can range widely – from as short as six weeks for minor procedures to as long as seven years (84 months) for more extensive treatments [11][13]. Many providers offer the flexibility of weekly, fortnightly, or monthly instalments, often aligned with your pay cycle via direct debit [5][7]. Below are some key considerations and examples to guide your planning.

2.1 Check Repayment Period and Instalments

Different providers cater to various budgets and treatment sizes, so it’s worth comparing options. For instance:

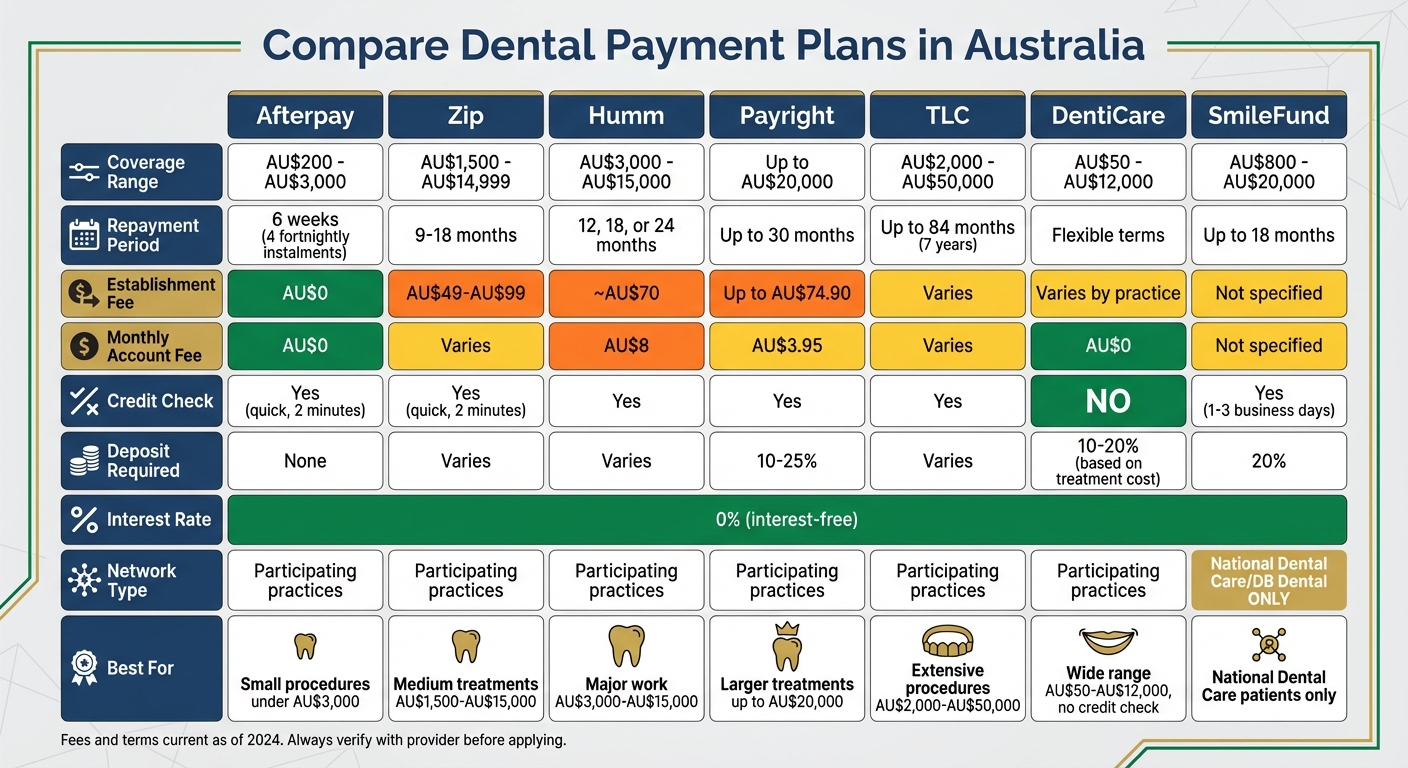

- Afterpay: Covers treatments between AU$200 and AU$3,000, with four fortnightly instalments over six weeks [11].

- Zip: Offers terms ranging from nine to 18 months for treatments costing between AU$1,500 and AU$14,999 [11].

- Humm: Provides 12-, 18-, or 24-month plans for procedures valued from AU$3,000 to AU$15,000 [11].

- Payright: Extends repayment terms up to 30 months for amounts as high as AU$20,000 [13].

- TLC: Offers personal loans ranging from AU$2,000 to AU$50,000, with repayment terms stretching up to 84 months [11][13].

Most plans are interest-free, meaning you only pay the treatment cost plus any administrative fees. However, keep an eye out for charges like establishment fees – for example, Zip (AU$49–AU$99), Humm (around AU$70), and Payright (up to AU$74.90) [11][13]. Monthly account fees can also apply, such as AU$3.95 for Payright or AU$8 for Humm [11][13]. On the bright side, many providers let you make early repayments or lump-sum contributions without penalties, which can shorten your repayment period [5][7].

2.2 Verify Interest-Free Period and What Happens After

While some plans remain interest-free for the entire term [1][12], others only offer an initial promotional period. If the balance isn’t cleared within this timeframe, interest may be applied to the remaining amount – and in some cases, it could even be backdated to the original loan date [14]. It’s essential to clarify whether the plan stays interest-free throughout or becomes interest-bearing after the promotional period.

Also, check what happens if you miss a payment. Many providers impose missed payment fees – for example, Openpay charges AU$9.50 [12]. Providers like DentiCare process direct debits from midnight on the scheduled date, so ensure funds are available the night before to avoid penalties [7]. If you’re struggling financially, ask your provider about hardship options, as many offer assistance programs [7].

2.3 Look for Flexible Repayment Structures

Flexibility can make a big difference, especially for larger treatments. Some providers allow adjustments to existing plans. For example, DentiCare lets practices modify instalment amounts or extend durations if your circumstances change [7]. They also offer tools like the DentiCare App, where you can track your balance and make extra payments, which usually reduce the overall repayment period rather than replacing upcoming instalments [5][7].

For significant procedures, SmileFund provides interest-free repayment options for up to 18 months on treatments valued at up to AU$20,000 [16]. Some providers even extend repayment terms to 24 months for treatments costing as much as AU$70,000 [15]. If you need to adjust your payment schedule, it’s best to contact your dental practice directly, as they typically manage changes through their provider portal [7].

3. Check Eligibility and Approval Criteria

Before selecting a payment plan, it’s important to understand the eligibility requirements. Generally, most providers require applicants to be at least 18 years old and either an Australian citizen or a permanent resident. Some plans, like SmileFund, also extend eligibility to New Zealand residents [7][16].

3.1 Know What Documentation and Credit Checks Are Required

When applying, you’ll need to provide standard identification and financial details. This typically includes a government-issued photo ID, such as a Driver’s Licence, that confirms your current address [3]. Providers also request your credit or debit card information and bank account details to set up direct debits [7]. Additionally, having a valid mobile number and email address is crucial for managing your application online [3].

Some providers have specific income and employment requirements. For example, DentiCare mandates current employment and does not accept Centrelink as a primary source of income [7]. Applicants must also confirm they haven’t been declared bankrupt or entered into a debt agreement in the last seven years [7]. If you’re applying for treatment-specific financing, you’ll need to provide a copy of your dental treatment plan from your dentist to finalise the loan amount [17].

Credit check policies vary by provider. DentiCare, which has supported over 280,000 patients, does not conduct credit checks [5]. On the other hand, SmileFund performs credit assessments, with approvals typically completed within one to three business days [17]. Providers like Afterpay and Zip Money offer quick credit checks that can be completed at the dental practice in about two minutes. These checks are not income-tested, making them more accessible [3].

3.2 Consider Providers that Minimise Credit Checks

If you’re concerned about the impact of credit checks, some providers offer options without extensive assessments. For instance, DentiCare and MySmilePlan do not conduct credit checks [1].

Even with no-credit-check plans, an upfront deposit is usually required. For treatments under AU$2,000, a 20% deposit is standard, while treatments exceeding AU$2,000 typically require a 10% deposit [3]. SmileFund is available for procedures costing over AU$800 [16], while DentiCare covers treatments ranging from AU$50 to AU$12,000 [7]. SmileFund offers financing for treatments up to AU$20,000 [16]. To streamline the process, check with your dental practice to see which providers they work with [1].

sbb-itb-2be92ed

4. Compare Provider Networks and Coverage Limits

Once you’ve confirmed your eligibility, the next step is to identify which providers and coverage limits work best for your treatment needs.

Not all payment plans are available at every dental clinic. Providers like DentiCare, Humm, and Afterpay require your dentist to be a participating partner. For instance, SmileFund is exclusively available at National Dental Care and DB Dental clinics [7][16]. To avoid surprises, check with your dentist or use the provider’s ‘Find a Dentist’ tool to confirm if your clinic is part of their network [1].

4.1 Check Provider Network Options

Payment plans generally fall into two categories: in-house financing offered directly by the dental clinic or third-party plans that require the clinic to be a registered partner [7]. It’s worth asking your dentist about the options they support. For example, smile.com.au works with a network of over 3,000 dentists across Australia, giving you plenty of flexibility [1]. In contrast, SmileFund restricts access to specific clinic groups [16]. Keep in mind that many dentists only offer payment plans for more expensive procedures, rather than for routine check-ups [1].

4.2 Review Annual or Per-Procedure Limits

Once you’ve confirmed network availability, take a close look at the coverage limits offered by each provider.

Coverage limits can vary widely. For example, DentiCare covers treatments ranging from $50 to $12,000 [7], while SmileFund offers up to $20,000 but requires a minimum treatment cost of $800 [16]. For larger procedures exceeding $15,000, SuperCare allows you to tap into your superannuation, with limits determined by your fund balance [11]. On the other hand, smile.com.au memberships don’t impose annual benefit caps, instead offering consistent fee reductions [18]. Choose a plan that aligns with your treatment costs – Afterpay is ideal for minor procedures under $3,000, while Humm or TLC are better suited for major work, covering amounts between $3,000 and $50,000.

4.3 Create a Comparison Table for Different Plans

A comparison table can make it easier to evaluate provider flexibility, out-of-pocket expenses, and coverage limits. Here’s an example:

| Provider | Coverage Limit (AU$) | Network Type | Deposit Required | Interest Rate |

|---|---|---|---|---|

| DentiCare | $50 – $12,000 | Participating Practices | Varies by practice | 0% |

| SmileFund | $800 – $20,000 | National Dental Care/DB Dental only | 20% | 0% |

| Afterpay | $200 – $3,000 | Participating Practices | None | 0% |

| smile.com.au | No limit (fee reduction) | 3,000+ Participating Dentists | None | N/A |

For expensive treatments, combining a dental membership like smile.com.au (which reduces fees by 15%–40%) with a payment plan can help lower your instalments [18]. This strategy makes it easier to afford costly procedures without straining your finances.

5. Review Waiting Periods and Plan Restrictions

Unlike private health insurance, interest-free dental payment plans usually skip waiting periods, meaning you can start treatment as soon as your application is approved [5][21]. That said, the approval process itself can vary – ranging from just a few minutes to several business days – depending on the provider and the size of your treatment costs [20]. It’s essential to examine any potential restrictions tied to the plan before committing.

5.1 Check Waiting Periods for Major Procedures

One big advantage of dental payment plans is that they typically allow you to access treatment immediately after approval, bypassing the long waits often associated with private insurance. For instance, dental insurance might impose a 12-month wait for major treatments like crowns, implants, or orthodontics [19]. In contrast, some payment plans, like National Dental Plan, can approve applications in minutes – whether done in-clinic or online [22]. SmileFund, on the other hand, promises a decision within one to three business days [16]. However, if your treatment costs exceed A$2,000, you may need to provide additional proof of income and expenses [20].

5.2 Identify Excluded Services

While these plans are great for covering expensive procedures, they often exclude routine, low-cost care. Most providers won’t finance treatments below A$500 to A$1,000 [6]. For example, SmileFund covers treatments priced between A$800 and A$20,000 [16], while DentiCare handles a range from A$50 to A$12,000 [7]. These plans are typically aimed at general dentistry (like root canals), cosmetic procedures (such as veneers or teeth whitening), and orthodontics (like Invisalign or braces) [6]. To avoid surprises, ensure your specific treatment meets the minimum cost requirements set by the provider.

5.3 Determine If Pre-Treatment Estimates Are Required

Most providers will ask for a detailed treatment plan from your dentist before approving your application. For instance, DentiCare requires the dental practice to send a "Treatment Proposal" via SMS, which you then complete to finalise the plan [7]. Similarly, SmileFund mandates a copy of your treatment plan as part of the application process [16]. Treatment can only begin after both the provider and dentist have signed off on the plan. To avoid delays, ask your dentist for a comprehensive treatment plan during your initial consultation. Make sure it meets the provider’s minimum cost threshold – usually between A$800 and A$1,000 [16][22]. Reviewing these details carefully will help you select the best payment plan for your situation.

Conclusion

Choosing the right dental payment plan comes down to understanding the key details: treatment costs, repayment terms, and eligibility requirements. Start by working out the total cost of your dental care, including any hidden fees or exclusions, and compare repayment structures across providers. If an interest-free period is on offer, weigh up its true value – these plans often come with establishment fees or monthly charges. Taking the time to understand your options can help you avoid unexpected costs and ensure the plan fits comfortably within your long-term budget.

"The only decision that is bound to be wrong is ignoring your dental needs, as you don’t want to pay for your dental work" [4].

Rushing into a decision without fully grasping the terms can lead to financial surprises. Before committing, confirm whether your dentist accepts the provider you’re considering or offers their own in-house plans. Some practices make things simpler by offering interest-free repayment schedules over 2–6 months, cutting out third-party providers entirely [2]. For larger loans – like those up to A$50,000 or A$55,000 – it’s wise to consult a financial adviser. They can help ensure the repayment structure works for your budget and prevents long-term debt.

At Complete Smiles Bella Vista (https://completesmilesbv.com.au), the team provides clear explanations of treatment costs and offers payment options tailored to your needs. Asking questions, requesting detailed quotes, and double-checking eligibility criteria are essential steps before signing any agreement.

Finally, consider paying more than the minimum monthly repayment to avoid stretching out financial strain unnecessarily [23]. With nearly one in five Australians delaying dental care due to cost concerns [2], finding a suitable payment plan can help you take care of both your oral health and your financial wellbeing.

FAQs

What factors should I consider when estimating the total cost of dental treatment?

When calculating the cost of dental treatment, several factors come into play. These include the fees for the specific procedures, the type and quality of materials used, and how complex the treatment is. Sometimes, additional procedures – like gum contouring or orthodontic work – can add to the overall expense.

It’s always a good idea to have an open conversation with your dentist about all potential costs to avoid any unexpected charges. If affordability is a concern, many clinics offer interest-free payment plans, which can make managing the cost much easier. It’s worth looking into these options if needed.

How do I check if my dentist accepts a specific dental payment plan?

To find out if your dentist accepts a specific dental payment plan, the simplest approach is to contact their office directly. Ask if they work with the payment plan provider or option you have in mind.

Additionally, some dental practices might offer their own in-house payment plans or have arrangements with certain providers. Make sure to ask about all the available choices so you can select a plan that aligns with both your budget and treatment requirements.

Are there any extra costs or exclusions in dental payment plans?

While many dental payment plans, including interest-free options, promote themselves as having no hidden fees or interest charges, it’s crucial to read the fine print. Pay close attention to any potential administrative fees, penalties for late payments, or exclusions that might limit coverage for specific treatments or services.

By thoroughly understanding the terms, you can select a payment plan that aligns with your needs and helps you avoid surprise expenses. If anything seems unclear, reach out to your dental provider for further explanation.

Related Blog Posts

- Flexible Payment Plans for Major Dental Work

- Transparent Dental Pricing Explained

- Cost Comparison: Implants, Bridges, and Dentures in 2025

- Tooth Decay Treatment Costs: Options Explained

Important Notice: Any surgical or invasive procedure carries risks. Before proceeding, you should seek a second opinion from an appropriately qualified health practitioner.

Individual results may vary. The information provided in this article is for educational purposes only and does not constitute medical advice.

Checkout Related Blogs

Get in touch with us

For more information, call us now to start feeling better. Or fill the form below to make appointment

The Latest News from Complete Smiles

How to Clean Clear Plastic Retainers

Checklist for Choosing Wearable Dental Devices

Checklist for Choosing Cloud AI Platforms in Dentistry

Complete Smiles Bella VistaAccepts All Major Health Funds, Including